FATF Recommendations 8 & 16: Key Updates You Need to Know

Breaking Down the Latest FATF Updates: What You Need to Know About Recommendations 8 & 16

The Financial Action Task Force (FATF) has made significant updates to two critical recommendations that will reshape how financial institutions and governments approach anti-money laundering (AML) and counter-terrorism financing (CTF).

Why was there a Need to update FATF Recommendations 16 & 8 Now?

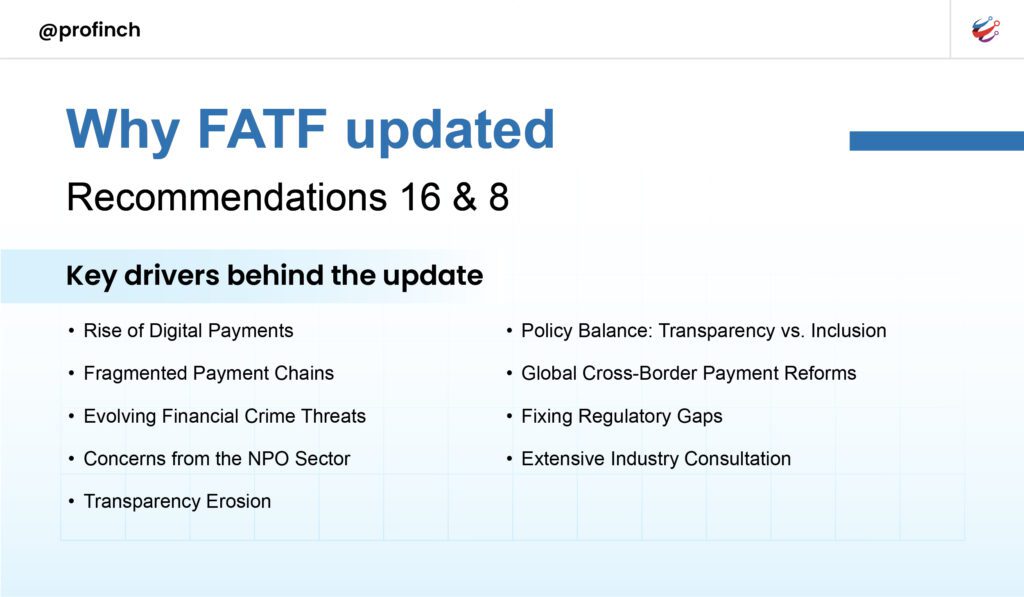

The update to FATF Recommendations was driven by several major developments and challenges in the payments landscape over the past decades:

- Rapid Evolution of Payment Technologies and Services

- Digital Payments Growth: The explosion of digital payment methods and cross-border transactions created new vulnerabilities.

- Cryptocurrency Concerns: The rising use of digital assets for illicit activities required better transparency measures.

- FinTech Innovation: New payment technologies needed updated regulatory frameworks

- Fragmented Payment Chains: With more players and intermediaries in the payment process, it has become harder for financial institutions to gather enough information to spot suspicious activities and comply with sanctions. Law enforcement agencies also face difficulties in accessing the necessary data to investigate financial crimes.

- Changing Financial Crime Risks: The nature of financial crime has shifted. Fraud is now a major predicate offense for money laundering, and there are growing concerns about proliferation financing (funding the spread of weapons of mass destruction). The update explicitly addresses these risks, expanding the focus beyond just terrorism financing.

- NPO Sector Pushback: Legitimate charities complained about excessive regulation hampering their work. And there was international pressure to protect civil society organizations from government overreach. Hence, we need to ensure charitable organizations can access banking services with minimal scrutiny wherever applicable and not all NPOs are high risk.

- Restoring Transparency: Transparency in payments has eroded due to the speed of technological change and the complexity of payment chains. The update aims to restore transparency by clarifying the roles and responsibilities of different parties and improving the quality of information shared in payment messages.

- Balancing Policy Objectives: The FATF wanted to ensure the new rules do not hinder financial inclusion, data protection, or the speed and cost-efficiency of payments. The revised recommendation reflects feedback from public consultations to strike a balance between transparency, privacy, and inclusion.

- Global Push for Better Cross-Border Payments: The update aligns with the G20 Priority Action Plan to make cross-border payments faster, cheaper, more transparent, and more inclusive, while maintaining safety and security.

- Addressing Gaps in Current Rules: Specific issues like the use of virtual account numbers (which can obscure the true location of funds) and the lack of transparency in cross-border cash withdrawals were identified as vulnerabilities that needed to be closed.

- Consultation and Stakeholder Feedback: The revision process included extensive consultation with industry and public stakeholders. Their input helped refine the rules to ensure they are practical, effective, and proportionate to the risks.

In summary, the FATF updated Recommendations to keep pace with technological advances, address new and evolving financial crime risks, restore transparency, and support global efforts to improve cross-border payments—all while ensuring the rules remain practical and do not unduly disrupt legitimate financial activity.

Key Changes to the Rules

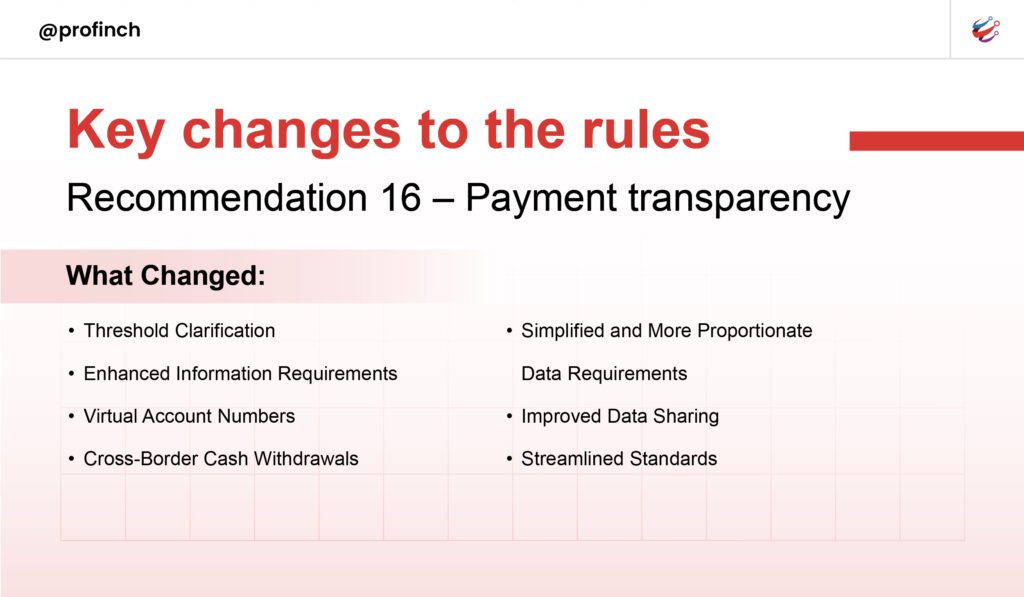

Recommendation 16 (Wire Transfers) – Payment Transparency

What Changed:

- Threshold Clarification: Cross-border payments over $1,000 USD/EUR now have stricter transparency requirements

- Enhanced Information Requirements: Financial institutions must collect and maintain more detailed information about the originator and beneficiary

- Virtual Account Numbers: The update prevents the use of virtual account numbers to hide the country of the account, ensuring authorities can trace where funds are held.

- Cross-Border Cash Withdrawals: A new framework requires financial institutions to provide cardholder names to acquiring banks within three business days of a request for cross-border cash withdrawals.

- Simplified and More Proportionate Data Requirements: Only the country and town name are now required for the beneficiary’s address, reducing privacy concerns and friction in payments. For originators, full address is required by default, but country and town will suffice if a full address isn’t available. Also, if a full date of birth isn’t available for the originator, just the year of birth is acceptable – helping maintain financial inclusion for those without full records.

- Improved Data Sharing: Better mechanisms for sharing payment information between countries and institutions

- Streamlined Standards: Simplified and more consistent requirements across jurisdictions

In Simple Terms: Think of this like requiring a detailed return address and recipient information on international packages worth over $1,000. Banks now need to know exactly who is sending money where and why, making it much harder for criminals to move money anonymously.

Recommendation 8 (Non-Profit Organizations) - Protecting Charities

What Changed:

- Focus on Fraud and Proliferation Financing: The objectives now explicitly target not only terrorism financing but also fraud and proliferation financing, reflecting the changing nature of financial crime.

- Risk-Based Implementation: Countries must assess actual terrorism financing risks rather than applying blanket measures to all NPOs

- Targeted Approach: Only NPOs that genuinely pose risks should face enhanced scrutiny

- Protection Measures: Explicit requirements to protect legitimate charitable organizations from overregulation

- Proportionate Response: Measures must be proportionate to the identified risk level

In Simple Terms: Instead of treating all charities like potential security threats, governments must now prove that specific organizations actually pose risks before imposing strict regulations. It’s like moving from searching every person at an airport to using risk-based screening.

What This Means for Different Stakeholders

For Banks and Financial Institutions:

- More detailed record-keeping requirements but clearer guidelines

- Investment in enhanced transaction monitoring systems

- Better international cooperation mechanisms

For Non-Profit Organizations:

- Reduced regulatory burden for low-risk charities

- A clearer understanding of compliance requirements

- Better protection from government overreach

For Governments:

- More sophisticated risk assessment capabilities required

- Need for balanced regulatory approaches

- Enhanced international cooperation obligations

For Businesses and Individuals:

- Slightly more information required for large international transfers

- Better protection of personal financial data

- More secure international payment systems

These updates represent FATF’s commitment to evolving with the times while maintaining robust protections against financial crime. The key message is clear: smart regulation, not just more regulation, is the path forward in the fight against money laundering and terrorism financing.

Curious how these changes affect your institution?

Connect with our experts today, to explore how Profinch can support your compliance strategy and implement the latest FATF guidelines effectively and with ease.